International Fraud Awareness Week is held annually every November. Helpful information on it can be found at fraudweek.com. This year, it talks about being a fraud fighter for your organization and that is all well and good. However, as consumers we need to be vigilant too and be our own fraud fighters to avoid being scammed and losing our hard-earned money.

Going on LinkedIn shows a lot is going on this fraud week with respect to many organizations and many tips as well from participants in supporting this special designated week for professionals involved in preventing fraud within their organizations.

BBC, the public broadcaster in the UK, has an active schedule of scam prevention programming. It is a good example of how they are embracing and supporting bringing awareness to the gravity of this international scourge which is impacting everyone. They kicked off their special fraud week on November 22nd and call it Scam Safe. Their programming is very comprehensive and impressive to say the least.

Two key words that seem to be mentioned and stressed in bringing attention to preventing fraud is the integrity of your systems and employees who are there to do everything possible to prevent scams from happening and a commitment to meet fraud head on as challenges continue to emerge through the employment of new technology (e.g., AI) to remove companies and individuals of their money.

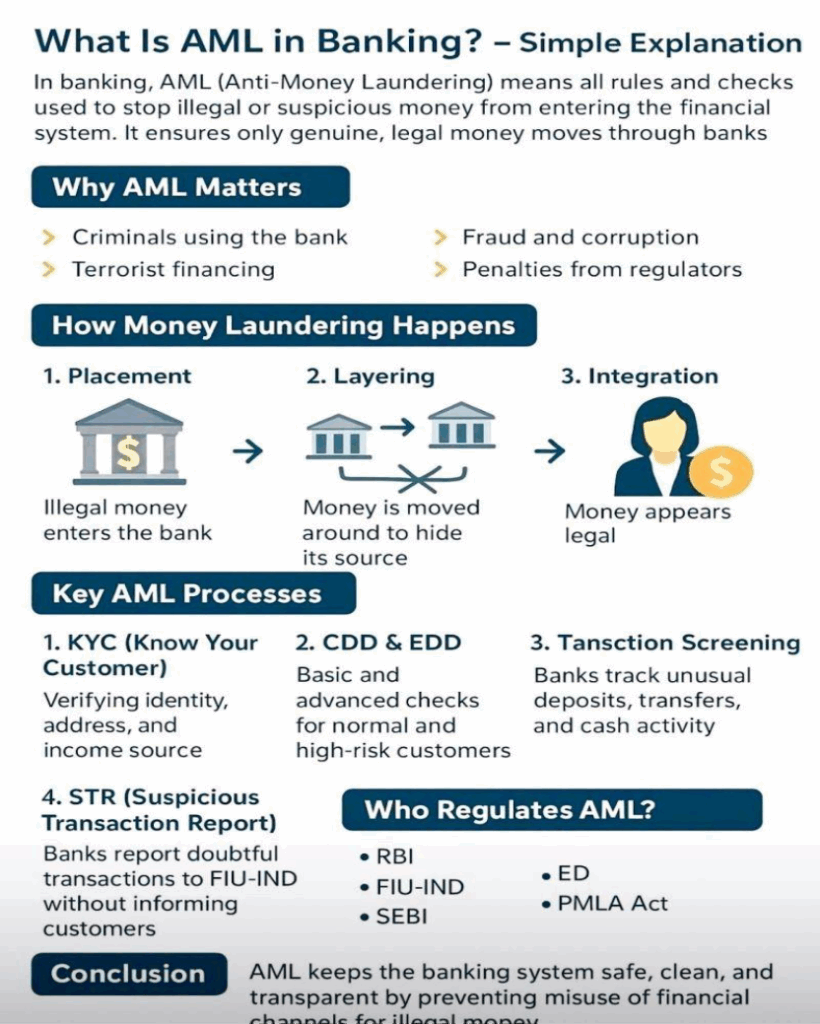

The posting below by anti-fraud specialist Ambika Sharma on LinkedIn is worth sharing here. The final statement on the chart below reads: channels for illegal money.

Understanding AML (Anti-Money Laundering) in Indian Banking – Made Simple!

Ambika Sharma | Associate Analyst | Skilled in KYC

AML refers to the framework of rules, checks, and monitoring systems that banks use to prevent criminals from hiding or moving illegal money through the financial system.

🔍 Why AML Matters ???

Strong AML practices help banks prevent:

• 🚫 Criminal misuse of banking channels

• 💣 Terrorist financing

• 🕵️♂️ Fraud, corruption & illicit activities

• ⚠️ Heavy regulatory penalties

🔄 How Money Laundering Works (3 Stages)

1. Placement – Introducing illegal money into the financial system.

2. Layering – Moving the money through multiple transactions to disguise its origin.

3. Integration – Bringing the laundered money back into the economy as “clean” funds.

🛡️ Key AML Processes

1. KYC (Know Your Customer) – Verifying customer identity, address & income source.

2. CDD / EDD – Basic and enhanced due diligence based on customer risk levels.

3. Transaction Monitoring – Identifying unusual deposits, transfers, or patterns.

4. STR Filing – Reporting suspicious transactions to FIU-IND discreetly (without informing the customer).

🇮🇳 Who Regulates AML in India?

• 🏦 RBI

• 🧾 FIU-IND

• 📈 SEBI

• 👮♂️ Enforcement Directorate (ED)

• ⚖️ PMLA Act (Prevention of Money Laundering Act)

✅ Conclusion

AML ensures that the financial system remains clean, transparent, and secure by preventing illegal money from entering or circulating within banks. Through KYC, due diligence, transaction monitoring, and STR reporting, banks play a crucial role in combating money laundering in India.

🔍 Demystifying Due Diligence: CDD, EDD, & AEDD

Shehan Edirisinghe | Assistant Manager | Banking & Financial Services

In the world of FinTech and Compliance, these acronyms are used constantly, but their roles and triggers are distinct. Understanding the difference is crucial for effective risk management and AML (Anti-Money Laundering) compliance.

1. 🔠 CDD: Customer Due Diligence (The Standard)

• What it is: The mandatory, foundational level of diligence applied to every single customer upon onboarding.

• Purpose: To verify the customer’s identity and assess the nature of their business relationship. It ensures you know who you’re dealing with.

• Key Components:

• Verifying the customer’s identity (KYC).

• Identifying the Ultimate Beneficial Owner (UBO).

• Understanding the purpose and intended nature of the business relationship.

2. 🚨 EDD: Enhanced Due Diligence (The Red Flag)

• What it is: A higher level of scrutiny applied to customers who present a higher risk of money laundering, terrorist financing, or other illicit activities.

• Trigger: Risk assessment flags, such as:

• The customer is a Politically Exposed Person (PEP).

• The business operates in a high-risk jurisdiction (e.g., sanctioned countries).

• The transaction involves unusual complexity or size.

• Key Components:

• More intensive background checks.

• Increased ongoing monitoring of transactions and activity.

• Deeper source of wealth/source of funds verification.

3. 📉 AEDD: Adverse Event Due Diligence (The Reaction)

• What it is: A specific, reactive form of due diligence performed after a potential adverse event or negative trigger has occurred or been identified. (Note: This term is less standardized than CDD/EDD and may be used interchangeably with ‘Triggered EDD’ or ‘Event-Driven Due Diligence’).

• Trigger: A change in the customer’s profile or status, such as:

• A customer appears on an adverse media report (e.g., being charged with a crime).

• A change in ownership or control is detected.

• Suspicious transaction monitoring alerts are consistently raised.

• Purpose: To reassess the customer’s risk profile based on new, negative information and determine if the relationship can continue.

The Takeaway:

CDD is your standard gate. EDD is your high-risk gate. AEDD is your post-event investigation that happens when a potential problem is identified.

What processes does your organization use to shift from CDD to EDD? Share your insights below!

hashtag#Compliance hashtag#AML hashtag#KYC hashtag#RiskManagement hashtag#DueDiligence hashtag#FinTech hashtag#RegTech