This LinkedIn post is quite revealing in showing our young adults make up a large share of those involved in setting up mule accounts to use for illegal purposes. How are they being detected and policed by our financial institutions?

If a large amount of money is coming into an account at one time or frequently even in smaller amounts, where is it all coming from? Likewise, if large amounts of money are then soon after being wired out from these mule accounts to international destinations, what controls are in place at a bank to ensure AML compliance is being adhered to.

Clearly this post is food for thought and points to weaknesses in our banking system if these mule accounts are being allowed to flourish alongside real-time payment growth. What are regulators doing about it to make sure our financial institutions are bringing in governance controls and measures to catch these younger adults setting up and using these accounts for fraud purposes?

After the fact detection is too late for all the victims of fraud. It is essential this mule account issue is dealt with to prevent fraud.

")

Gopal Chandra Sarkar

Banking & Financial Services Expert | Governance, Risk &

Compliance (GRC) Specialist

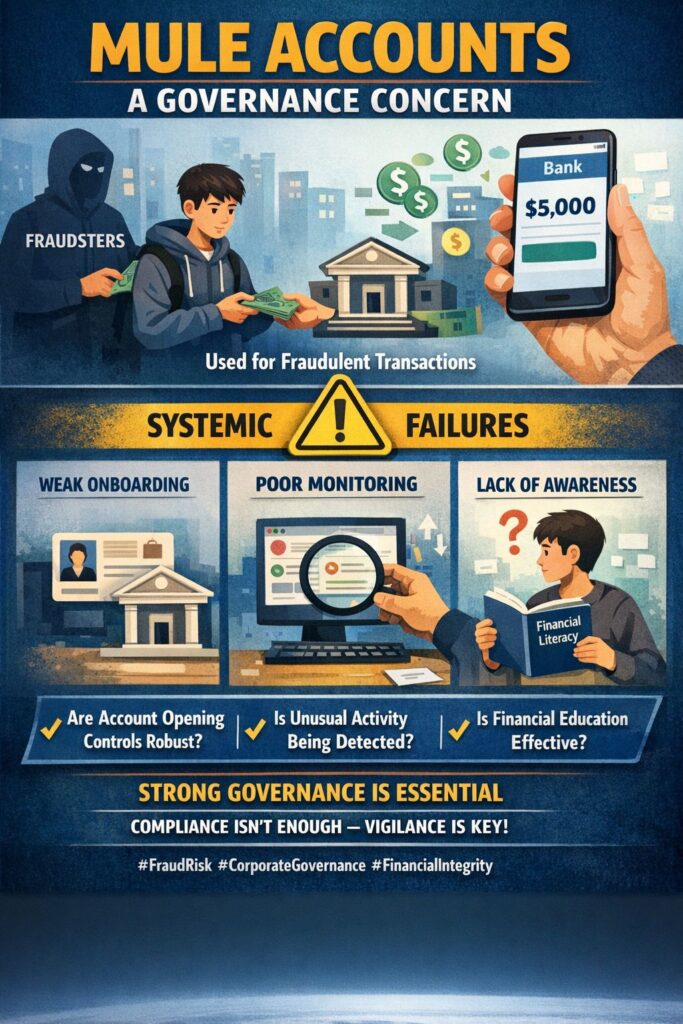

Post 2/8: Mule Accounts – A Silent Governance Breakdown?

What if the biggest fraud risk isn’t sophisticated hacking… but ordinary bank accounts being misused?

Mule accounts are quietly powering one of the fastest-growing segments of digital fraud.

🔍 Consider this:

Estimates suggest over 60–70% of financial fraud cases globally involve mule accounts at some stage

In many jurisdictions, young adults (18–30) form a significant share of identified mule account holders

Banks report a sharp rise in mule activity alongside real-time payments growth

But here’s the uncomfortable question:

Is this just a fraud issue… or a governance failure?

Ask yourself:

Are our account opening controls truly filtering risk—or just ticking boxes?

Are transaction monitoring systems flagging anomalies in real time—or after the damage is done?

Are financial literacy efforts strong enough—or are we leaving vulnerable groups exposed?

Because mule accounts don’t just enable fraud—

they expose systemic gaps across onboarding, monitoring, and awareness frameworks.

And that leads to a tougher boardroom question:

Are we governing risk proactively—or explaining it after the fact?

Prevention isn’t just compliance anymore.

It’s a test of governance vigilance in a real-time economy.

hashtag#FraudRisk hashtag#CorporateGovernance hashtag#FinancialIntegrity