It is clear in this LinkedIn post by Rishabh Gupta that a financial institution needs to not only be doing a proper job and carrying out its responsibility by exercising due diligence in onboarding a new customer, but moreover, it is an ongoing process which should never stop given life changes and the evolving nature of banking with all of its fraud implications so apparent in this era of AI digital fraud.

The bottom line is not only protecting the customer but preventing money from being stolen from them and going into proceeds of crime. As stated at the end of Mr. Gupta’s simplified AML onboarding flow, periodic KYC reviews and continuous monitoring is required.

")

Rishabh Gupta

Senior Fraud Analyst| Bank of America GBS |Approved by Financial Crime Academy

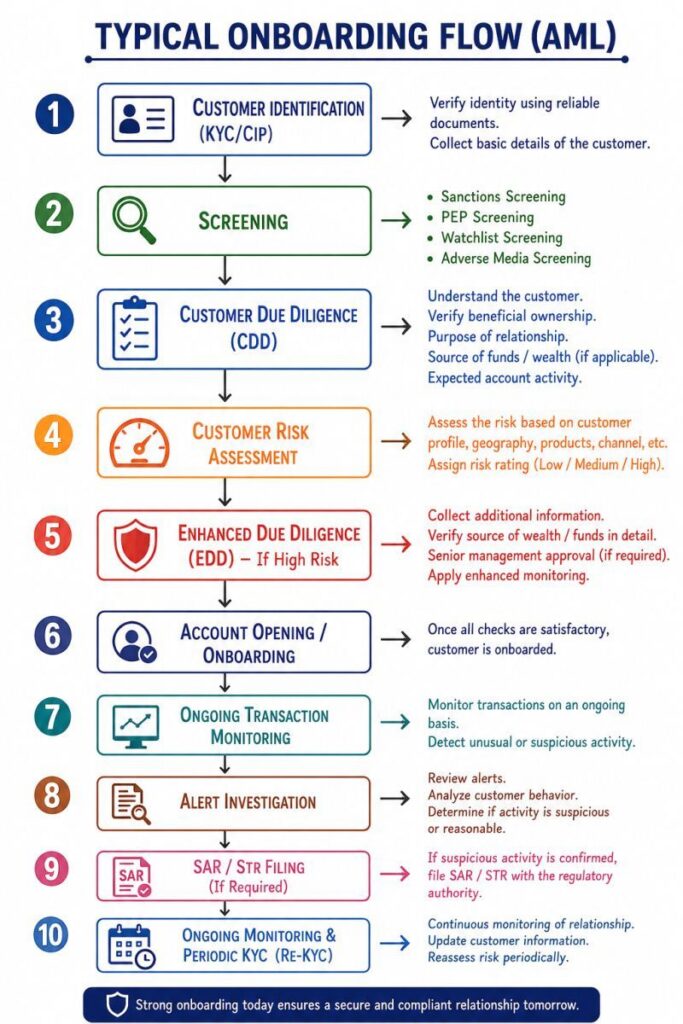

Understanding the AML Customer Onboarding Journey

Every successful customer relationship starts with a strong compliance foundation.

AML onboarding isn’t just about verifying identity. It’s about understanding who the customer is, assessing risk, and ensuring financial institutions remain protected from money laundering, fraud, terrorist financing, and other financial crimes.

Here’s a simplified overview of the Typical AML Onboarding Flow:

✅ Customer Identification (KYC/CIP)

✅ Sanctions, PEP & Adverse Media Screening

✅ Customer Due Diligence (CDD)

✅ Customer Risk Assessment

✅ Enhanced Due Diligence (EDD) for High-Risk Customers

✅ Account Opening & Onboarding

✅ Ongoing Transaction Monitoring

✅ Alert Investigation

✅ SAR/STR Filing (where required)

✅ Periodic KYC Reviews & Continuous Monitoring

While the exact process may vary across organizations and regulatory jurisdictions, these are the core building blocks of an effective AML compliance framework.

#AML #KYC #CDD #EDD #FinancialCrime #Compliance #RiskManagement #TransactionMonitoring #Sanctions #PEPScreening #AMLCompliance #Banking #FinCrime #RiskAnalyst #Learning #CareerGrowth